Monetization project | Acko Insurance

Determining the optimal point to charge Core and Power Users by identifying Aha Moments (when users first experience core value) and Happy Moments (when users experience recurring value), ensuring Perceived Value exceeds Perceived Price.

Identifying Which Aspect Determines Value for Your Product

I’ll determine the aspects of Acko’s insurance product (policies) that provide the most significant benefits to Core Users (Frequent Policy Managers, e.g., Bhakti, Lalit) and Power Users (Reward-Driven Users), using the four goal types: Functional, Personal, Financial, and Social.

- Functional Goal:

- Core Users: Manage policies seamlessly (e.g., check status, renewals, add family details) via the app, reducing the hassle of traditional insurance processes (e.g., paperwork, agent visits).

- Power Users: File claims quickly (24-hour settlements) and manage multiple policies (e.g., vehicle + health) in one app, streamlining insurance tasks.

- Value: Acko’s paperless, app-based process (per CVP: “simple, fast, paperless”) saves time and effort, a key functional benefit.

- Personal Goal:

- Both Segments: Gain peace of mind through reliable insurance coverage (e.g., 100% cashless, 24-hour claims), ensuring protection for what matters (e.g., family, vehicle).

- Value: Acko’s CVP (“Protect what matters”) and trust signals (78M+ users, 4.6 rating) provide emotional security, enhancing quality of life.

- Financial Goal:

- Core Users: Save money through loyalty discounts (e.g., 10% off after 1 year, per prior step) and NCB (e.g., 20% after 1 claim-free year).

- Power Users: Maximize savings with higher discounts (e.g., 25% off after 3 years), NCB (up to 50%), and rewards (e.g., via CRED partnership).

- Value: Acko’s discounts and rewards (per Medium article) directly address India’s price-sensitive market, offering financial benefits.

Primary Value Aspect: The most significant benefit for Core and Power Users is the Financial Goal (saving money through discounts, NCB) and Functional Goal (convenience of a paperless, app-based process with 24-hour claims). These align with Acko’s CVP (“affordable, instant insurance”) and user priorities (e.g., Bhakti, Lalit: convenience; Power Users: rewards).

Competitor Benchmarking

I’ll assess Acko’s benefits against competitors (e.g., LIC, Policybazaar) to identify differentiation, value at similar/lower pricing, and the next best alternative.

Aspect | Acko Insurance | LIC (Traditional Insurer) | Policybazaar (Aggregator) | Differentiation/Value Offered |

|---|---|---|---|---|

Claim Settlement Speed | 24-hour settlements, 100% cashless. | 7-15 days, partial cashless. | 3-5 days, varies by provider. | Acko’s fastest claims (24 hours) save time, a key functional benefit. |

Process Convenience | Paperless, app-based management. | Requires paperwork, in-person visits. | App-based but often needs agent support. | Acko’s fully digital process offers superior convenience. |

Pricing/Discounts | Loyalty discounts (e.g., tiered, NCB), competitive premiums (market avg ~₹5,000). | Higher premiums, limited discounts. | Aggregates competitive prices, some discounts. | Acko offers better savings via loyalty discounts (e.g., NCB, CRED rewards). |

Trust | 78M+ users, 4.6 rating, digital-first. | High legacy trust, slower processes. | 4.5 rating, aggregator trust. | Acko matches digital trust, but LIC has stronger legacy trust. |

- Do Benefits Match?: Acko matches Policybazaar on digital convenience and competitive pricing but exceeds both LIC and Policybazaar on claim speed (24 hours vs. 3-15 days) and paperless processes.

- What’s Different?: Acko’s 24-hour claim settlements and loyalty-driven discounts (e.g., tiered, NCB) provide more functional (time savings) and financial (cost savings) value than competitors.

- More Value at Similar/Lower Offering?: Acko can offer more value (faster claims, better discounts) at a similar market price (~₹5,000 annual premium), making it attractive to Core and Power Users.

- Next Best Alternative: If not Acko, Policybazaar is the next best alternative due to its competitive pricing and digital interface, though it lacks Acko’s speed and discount depth.

Quantify Results Ensuring Alignment with Price

I’ll quantify the Perceived Value for Core and Power Users based on the primary aspects (Financial and Functional Goals), ensuring alignment with the Perceived Price (market avg ~₹5,000 annual premium).

- Financial Goal (Money Saved):

- Core Users: Loyalty discounts (e.g., 10% off after 1 year) and NCB (e.g., 20% after 1 claim-free year) save ~₹1,500 annually on a ₹5,000 premium (assuming combined discounts).

- Power Users: Higher discounts (e.g., 25% off after 3 years), NCB (up to 50%), and CRED rewards (e.g., 5%) save ~₹3,000 annually on a ₹5,000 premium.

- Quantified Value: Core Users: ₹1,500 saved/year; Power Users: ₹3,000 saved/year.

- Functional Goal (Time Saved):

- Claim Filing: Acko’s 24-hour claim settlement vs. Policybazaar (3-5 days) or LIC (7-15 days) saves ~5-10 days per claim. Assuming 1 claim/year, this is ~5-10 days saved annually.

- Policy Management: Paperless process saves ~2 hours per interaction (e.g., renewals, cross-sells) vs. traditional methods (LIC: 4-5 hours with paperwork). Core Users (2 interactions/year) save ~4 hours; Power Users (4 interactions/year) save ~8 hours.

- Quantified Value: Core Users: 5 days (claims) + 4 hours (management); Power Users: 10 days (claims) + 8 hours (management).

Mapping Perceived Value Across the User Journey

Homepage

- Content: The homepage greets the user ("Hey Dhruv") and offers quick access to "Your Acko Essentials" (Policies, Vehicles, Family, Rewards) and an "Explore Insurance" section with a car insurance offer ("Get up to 85% off on car insurance", "Save as much as ₹40,000").

- Perceived Value:

- Convenience: Centralized access to essential features (policies, vehicles, etc.) simplifies user navigation.

- Cost Savings: The car insurance offer highlights significant savings (up to 85% off, ₹40,000), appealing to cost-conscious users.

- Aha Moment: The Aha Moment here is the realization of potential cost savings on car insurance. The prominent discount ("Get up to 85% off") and specific savings amount (₹40,000) create a strong first impression of value, encouraging the user to explore further.

The Home Page does not hold back in highlighting the benefits & discounts which increase the chances of users taking the next step!!

Health Insurance Exploration

- Content: The user navigates to explore Acko’s health plans, seeing a discounted premium ("Flat 15% off", ₹1,508/yr with ‘APP15’ coupon). Benefits include access to 10,500+ cashless hospitals and no limit on hospital room rent.

- Perceived Value:

- Affordability: The 15% discount reduces the premium to ₹1,508/yr, making the plan seem cost-effective.

- Comprehensive Coverage: Access to a large network of cashless hospitals and no room rent limit signals robust coverage, addressing key user concerns (hospital expenses, flexibility).

- Aha Moment: If the user didn’t experience the Aha Moment on the homepage, this could be it. The discounted price combined with clear, valuable benefits (cashless hospitals, no room rent limit) delivers the first core value experience for health insurance.

- Happy Moment: The application of the ‘APP15’ coupon (₹1,508/yr) is a Happy Moment. It provides recurring value by reinforcing the affordability of the plan, making the user feel rewarded for choosing Acko.

As you continue, on the home page, a discount coupon pops up & it's already applied, which also clearly reflects the money saved! An "AHA" moment!.

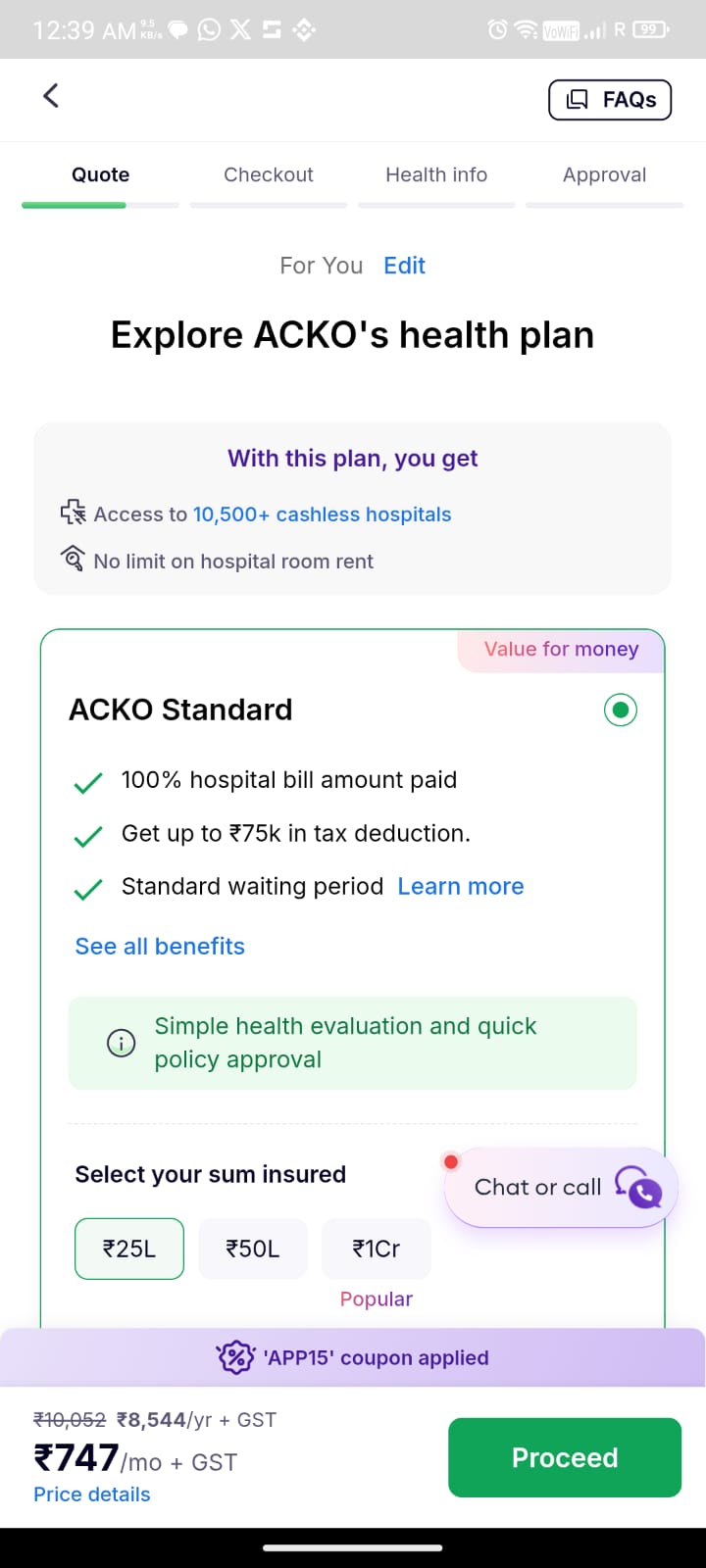

Health Plan Details

- Content: The user selects a plan (sum insured options: ₹25L, ₹50L, ₹1Cr) and sees detailed benefits of the "Acko Standard" plan: 100% hospital bill coverage, no copay, no room rent limit, 10% added inflation protection, and standard waiting periods (30 days initial, 2 years for specific illnesses, 3 years for pre-existing diseases).

- Perceived Value:

- Transparency: Clear breakdown of benefits (100% bill coverage, no copay) builds trust.

- Financial Security: Features like inflation protection and no copay reduce future financial burdens.

- Flexibility: Multiple sum insured options cater to different needs.

- Aha Moment: If not already experienced, the detailed benefits (e.g., 100% bill coverage, no copay) could be the Aha Moment, as they directly address common pain points in health insurance (out-of-pocket expenses, hidden costs).

- Happy Moment: The ability to customize the sum insured (₹25L, ₹50L, ₹1Cr) is a Happy Moment. It provides recurring value by empowering the user to tailor the plan to their needs, enhancing their sense of control and satisfaction.

Comparison with Market Plans

Comparison with Market Plans

- Content: A comparison table shows why the "Acko Standard Health Plan" is better than other market plans: 100% hospital bill payment (vs. ~85%), no copay (vs. fixed copay), no room rent limit (vs. extra payment for upgrades), 10% added inflation protection (vs. none), and equal waiting periods.

- Perceived Value:

- Superiority: Acko’s plan is positioned as better than competitors, increasing its perceived value.

- Trust: The comparison addresses user concerns (copays, room rent limits), making Acko seem more reliable.

- Aha Moment: For users comparing plans, this could be the Aha Moment. The clear superiority of Acko’s plan over others (e.g., 100% bill coverage vs. 85%) solidifies its value proposition.

- Happy Moment: The reassurance of choosing a better plan (e.g., no copay, inflation protection) is a Happy Moment. It provides recurring value by confirming the user’s decision, reducing buyer’s remorse.

There's also a very clear comparison of advantages and features between Acko & others - eliminates mental blockers of a user

FAQs and Support

- Content: The user sees a "Got questions? Find answers" section with FAQs (e.g., coverage for pre-existing conditions, OPD expenses, maternity) and a "Chat or call" option. There’s also a prompt to upgrade to "Acko Platinum" for better coverage.

- Perceived Value:

- Support: Access to FAQs and live support (chat/call) enhances user confidence.

- Upsell Opportunity: The "Acko Platinum" upgrade suggests even greater value for those seeking premium coverage.

- Happy Moment: The availability of instant support via "Chat or call" and relevant FAQs is a Happy Moment. It provides recurring value by ensuring users can resolve doubts quickly, enhancing their experience and trust in Acko.

The page also addresses FAQs that users might have!

Given Acko’s nature as an insurance company with dynamic premiums and coverage, I’ve analyzed the existing pricing for various insurance & analyzed the design in the proposed a redesign, and provided reasoning for the changes.

Analysis of Existing Pricing Pages - I have taken the pricing part of the 2 insurance policies (Health & Bike)

HEALTH PLAN

Health Insurance Pricing Page

The screenshot shows a pricing details popup with a breakdown of the premium, discounts, and total cost.

Current Design Elements:

- Pricing Breakdown:

- Yearly premium: ₹10,052.45

- Discount ("APP15" applied): ₹8,544.59

- GST (18%): ₹1,538.02

- Total: ₹10,082.61/year (or ₹882.22/month)

- Additional Information:

- Note: Discount applies yearly.

- Monthly payment option available.

- CTA (Call to Action):

- Green "Okay" button to confirm and proceed.

- Context:

- Part of the "Explore Acko’s Health Plan" flow, with tabs like "Quote," "Checkout," "Health Info," and "Approval."

Strengths:

- Transparency: Detailed breakdown of premium, discount, and GST builds trust.

- Flexibility: Monthly payment option caters to varied budgets.

- Clarity: Note about recurring discounts ensures user understanding.

Weaknesses:

- Static Display: Pricing is presented as a final figure without interactive elements.

- CTA Visibility: "Okay" button lacks emphasis, potentially reducing conversion.

- Lack of Context: Users may not see how inputs (e.g., age, coverage) affect the price.

Purpose of Current Design:

- Trust Building: Clear cost breakdown addresses user skepticism in insurance purchases.

- Simplification: Static popup ensures users focus on the final cost without distractions.

- Progression: Part of a guided flow to keep users moving toward purchase.

Redesigning the page

Redesigned Layout:

- Header:

- "Your Health Plan Price Breakdown" with a progress bar (e.g., Quote → Customize → Checkout).

- Interactive Calculator Section:

- Inputs: Age, number of family members, pre-existing conditions (dropdowns).

- Live Update: Premium adjusts in real time (e.g., "Base: ₹10,052 → ₹12,000 with family").

- Pricing Card:

- Breakdown:

- Base Premium: ₹10,052.45

- Discount ("APP15"): -₹1,507.86 (15% off)

- Net Amount: ₹8,544.59

- GST (18%): ₹1,538.02

- Total: ₹10,082.61/year (or ₹882.22/month)

- Toggle: Switch between yearly/monthly pricing.

- Discount Section:

- "Applied: APP15 (₹1,507 saved)" with an "Add Coupon" field.

- Educational Tooltips:

- Hover on "GST" or "Net Amount" for explanations (e.g., "GST is an 18% tax on the net premium").

- CTA:

- Bright orange "Proceed to Checkout" button with a smaller "Edit Plan" link.

- Colors: Green for savings, orange for CTA, neutral gray for informational text.

Reasoning for the Redesign

- Interactive Calculator:

- Why: Allows users to see how their inputs (e.g., family size) affect pricing, reflecting Acko’s dynamic pricing model.

- Impact: Enhances transparency and control, reducing purchase hesitation.

- Pricing Toggle:

- Why: Yearly vs. monthly view caters to different budgeting preferences.

- Impact: Increases flexibility, appealing to a broader audience.

- Educational Tooltips:

- Why: Terms like GST can confuse users; tooltips educate without clutter.

- Impact: Boosts confidence, especially for first-time buyers.

- Bold CTA:

- Why: Orange "Proceed to Checkout" grabs attention over the neutral "Okay."

- Impact: Drives higher conversions by guiding users clearly.

BIKE INSURANCE

Bike Insurance Pricing Page

The screenshot shows a screen with bike insurance options, including tenure, plan types, and pricing.

Current Design Elements:

- Vehicle Details:

- IDV (Insured Declared Value): ₹62,500 (editable).

- Tenure Options:

- 1 Year, 2 Years (Save ₹154), 3 Years (Save ₹404).

- Plan Types:

- Comprehensive Plan: ₹1,953 (covers bike damage, third-party liability, cashless claims at 5400+ garages).

- Own Damage Plan: ₹587 (covers bike damage, cashless claims).

- Discount:

- "APP150" applied, saving ₹150.

- Total Cost:

- ₹1,953 + 18% GST for Comprehensive Plan.

- CTA:

- Green "Continue" button.

Strengths:

- Customization: Editable IDV and tenure options reflect dynamic pricing.

- Incentives: Tenure-based savings encourage longer commitments.

- Service Highlight: Cashless claims at 5400+ garages add value.

Weaknesses:

- Lack of Interactivity: Premium doesn’t update live as users adjust options.

- Minimal Breakdown: GST is mentioned, but no detailed cost split.

- Feature Overlap: Plan differences (e.g., third-party liability) aren’t visually distinct.

Purpose of Current Design:

- Flexibility: Editable fields allow tailored pricing for diverse users.

- Value Perception: Savings on longer tenures nudge users toward higher-value plans.

- Simplicity: Single-screen flow minimizes friction in decision-making.

Redesigning the page

- Header:

- "Customize Your Bike Insurance Plan" with a progress bar (Vehicle → Coverage → Add-ons).

- Step 1: Vehicle Details (Collapsible):

- Inputs: Make, model, year, registration number.

- IDV Slider: ₹50,000–₹100,000 (default: ₹62,500).

- Live IDV impact on premium (e.g., "IDV: ₹62,500 → Premium: ₹1,953").

- Step 2: Coverage Selection:

- Plan Cards:

- Comprehensive: ₹1,953 (Icons: Bike Damage, Third-Party, Cashless Claims).

- Own Damage: ₹587 (icons: Bike Damage, Cashless Claims).

- Tenure Tabs:

- 1 Year: ₹1,953 | 2 Years: ₹3,752 (Save ₹154) | 3 Years: ₹5,450 (Save ₹404).

- Step 3: Add-ons & Discounts:

- Checkboxes: Zero Depreciation (+₹300), Roadside Assistance (+₹150).

- Discount Field: "APP150" applied (₹150 off).

- Live Total: ₹1,953 → ₹2,253 (with add-ons) → ₹2,103 (after discount).

- Pricing Summary:

- Base: ₹1,953 | Add-ons: ₹300 | Discount: -₹150 | GST (18%): ₹351 | Total: ₹2,454.

- CTA:

- Bright orange "Proceed to Payment" button.

Visual Elements:

- Colors: Green for savings/add-ons, orange for CTA, blue for tenure tabs.

Reasoning for the Redesign

- Wizard Flow with Progress Bar:

- Why: Breaks down decisions (vehicle → coverage → add-ons) into manageable steps.

- Impact: Reduces cognitive load, improving user experience.

- IDV Slider with Live Updates:

- Why: Immediate premium adjustments as IDV changes show pricing logic.

- Impact: Builds trust through transparency and interactivity.

- Visual Plan Cards:

- Why: Icons and clear differentiation make plan benefits scannable.

- Impact: Simplifies decision-making for non-expert users.

- Tenure Savings Visualization:

- Why: Highlighting savings (e.g., "Save ₹404") encourages longer tenures.

- Impact: Increases customer lifetime value for Acko.

- Add-ons and Discounts:

- Why: Live updates on add-ons and discounts clarify cost impacts.

- Impact: Encourages upselling (add-ons) and conversions (discounts).

Summary Table: Key Changes and Benefits

Section | Original Feature | Redesigned Feature | Benefit |

|---|---|---|---|

Health - Pricing | Static breakdown (₹10,082.61) | Interactive calculator + toggle | Transparency, user control |

Health - CTA | Green "Okay" button | Orange "Proceed to Checkout" | Higher visibility, better conversion |

Bike - Flow | Single screen, static | Wizard with progress bar | Reduced complexity, guided process |

Bike - Pricing | No live updates | IDV slider, live premium updates | Transparency, interactivity |

Bike - Plans | Text-based plan details | Visual cards with icons | Easier comprehension, faster choice |

Brand focused courses

Great brands aren't built on clicks. They're built on trust. Craft narratives that resonate, campaigns that stand out, and brands that last.

All courses

Master every lever of growth — from acquisition to retention, data to events. Pick a course, go deep, and apply it to your business right away.

Explore courses by GrowthX

Built by Leaders From Amazon, CRED, Zepto, Hindustan Unilever, Flipkart, paytm & more

Course

Advanced Growth Strategy

Core principles to distribution, user onboarding, retention & monetisation.

58 modules

21 hours

Course

Go to Market

Learn to implement lean, balanced & all out GTM strategies while getting stakeholder buy-in.

17 modules

1 hour

Course

Brand Led Growth

Design your brand wedge & implement it across every customer touchpoint.

15 modules

2 hours

Course

Event Led Growth

Design an end to end strategy to create events that drive revenue growth.

48 modules

1 hour

Course

Growth Model Design

Learn how to break down your North Star metric into actionable input levers and prioritise them.

9 modules

1 hour

Course

Building Growth Teams

Learn how to design your team blueprint, attract, hire & retain great talent

24 modules

1 hour

Course

Data Led Growth

Learn the science of RCA & experimentation design to drive real revenue impact.

12 modules

2 hours

Course

Email marketing

Learn how to set up email as a channel and build the 0 → 1 strategy for email marketing

12 modules

1 hour

Course

Partnership Led Growth

Design product integrations & channel partnerships to drive revenue impact.

27 modules

1 hour

Course

Tech for Growth

Learn to ship better products with engineering & take informed trade-offs.

14 modules

2 hours

Crack a new job or a promotion with ELEVATE

Designed for mid-senior & leadership roles across growth, product, marketing, strategy & business

Learning Resources

Browse 500+ case studies, articles & resources the learning resources that you won't find on the internet.

Patience—you’re about to be impressed.